-- Active Funds Gain An Edge In 2024's First Half

Past Viewpoints:Update: Is Tax-Efficiency Largely A Myth?

Ben Franklin summed it up nicely: "…in this world nothing can be said to be certain except death and taxes."

Under today’s tax code, the more money your portfolio makes, the more taxes you will ultimately have to pay. You can pay it now, or you can pay it later. If you pay it later, tax rates may be higher than they are now, because at some point the interest on the Federal debt will need to be fully serviced.

While there are a few ways to be truly tax-efficient, limitations and trade-offs loom large. The following are listed in descending order of potential usefulness:

- Contribute to a retirement account during your working years if possible. Traditional retirement plans allow you to start with pre-tax money and enjoy tax-free compounding, with taxes levied only when distributions occur. Roth accounts require after-tax contributions but do not get taxed again.

- Hold a low turnover index position (such as Total Market Index) in a taxable account for your entire life, with plans to have your heirs pay any estate taxes that come due (and hope there will be very little or none due).

- Offset income, retirement account distributions, and capital gains tax by donating highly-appreciated taxable holding(s) to Fidelity Charitable (or some other donor advised fund). This can make sense if you plan to make sizable grants to IRS-registered charities in future years.

- Invest in Municipal Bonds. Tax-free income sounds great, but yields are lower than taxable bond funds, so the tax benefit is marginal at best. Worse, durations for most state-specific funds are relatively high, meaning that any additional rise in long-term interest rates could lead to capital losses.

- Obtain poor investment results – perhaps by attempting to time the market. You can laugh at this one, but remember it the next time you encounter a firm that is bragging about their tax-efficiency. It’s easy to keep taxes low when you have lots of losses available to harvest.

Apart from these options, tax-efficiency is more illusion than reality. Many promoters of " tax-advantaged" vehicles are simply employing delay (deferral) tactics. By minimizing capital gain distributions and harvesting losses from bad bets, these vehicles allow an investor to build up a large unrealized gain over time, much like holding an individual stock. This keeps taxes low during the holding period, but then you make up for it later when you sell the position. Once the gain is realized, the total taxes paid are much the same as any other active vehicle (with the same total return) that may have distributed more long-term capital gains along the way.

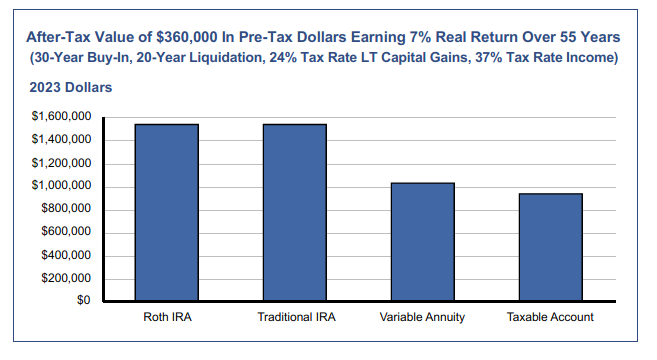

Then there’s the lure of tax-free compounding with variable annuities. Problem is, you’ve already paid taxes on the money once, and now you get to do it again on future gains – at full income rates upon withdrawal, much like a Traditional IRA. The only way to get ahead of a taxable account is to take on the full risk of the stock market for a deferral period of at least two decades (that’s not how most variable annuities are positioned, but the result is shown below).

The chart below shows the after-tax liquidated value of different tax-deferral vehicles at the indicated tax rate. Traditional IRAs, Roth IRAs, and taxable accounts only get taxed once on their gains. Roth money is taxed up-front before contributions; Traditional IRAs are taxed all at once upon withdrawal. Taxable accounts are taxed each year on distributed income and capital gains, and on any remaining gains whenever a position is sold.

This brings us to perhaps the single most important thing you can do to maximize after-tax performance (provided you have both retirement accounts and taxable accounts): use your retirement accounts for more aggressive stock-oriented strategies, and use your taxable account(s) for more conservative lower-risk strategies where bonds and/or cash are part of the mix. This may seem counterintuitive to some investors, given the higher tax rate on income relative to long-term capital gains. But over the long run, stocks are likely to exceed inflation by 7 percentage points annually, whereas bonds may only deliver a 3-4 percentage point advantage in the coming decades. Clearly, the tax burden created by bond-oriented investments will be significantly smaller than that of stocks, and bonds may create more opportunities for tax-loss harvesting as well. For those reasons, we think it’s better to use a taxable account for lower-return strategies.

Third Quarter ReviewRising interest rates moved to the top of the 2023 concerns list in the third quarter, tempering market enthusiasm for the long-coveted soft landing and any economic benefits that the Artificial Intelligence (AI) revolution might bring. Also adding to the somber mood: other central banks around the world declared victory over inflation at lower peak rates than the U.S., which caused the dollar to gain strength. That could slow future earning growth - especially for global technology disruptors.

Progress on inflation was threatened by higher oil prices and wage demands. With OPEC+ agreeing to cut crude production in the face of continuing strong demand for leisure travel, oil prices surged during the third quarter – prompting speculation that the Fed may not be done hiking interest rates until sometime early next year. Generous wage agreements for unionized employees, along with the recent walkouts organized by the UAW also prompted worries that wage inflation could become a longer-term problem.

For the third quarter the S&P 500 declined 3.3% to finish with a 13.1% year-to-date gain. On the bond side, the Bloomberg Barclay's U.S. Aggregate pulled back 3.2% for a 1.0% loss on a year-to-date basis. Performance-wise, the stock side of our portfolios generally declined in tandem with the S&P 500, although our sector allocation performed slightly worse, narrowing its year-to-lead over the index. We managed to outperform on the bond side, limiting our losses relative to the Bloomberg Barclays U.S. Aggregate Index as a result of our continuing emphasis on shorter-term debt (which in some cases included the upper tiers of the high-yield segment).

OutlookThe rising price of oil is somewhat worrisome, but it tends to boost GDP because the U.S. exports more than it imports. On the inflation front, rising energy costs are somewhat mitigated by the weakening housing sector and declining rents. The main concern is that inflation may stop improving, which would leave it well above the Fed’s 2% target. But we don’t see high oil prices as a long-lasting situation. China’s excess oil demand will likely be eliminated in the fourth quarter when its strategic reserve is filled to the brim. And in most of the world’s major automotive markets, vehicle miles traveled for internal combustion vehicles is declining due to aging populations and because global miles driven in battery-electric vehicles is now about 2% and climbing rapidly.

Concerns about rising wages may be overblown. A surge in productivity is allowing businesses and factories to absorb most of the increase, limiting the amount that is passed on in the form of higher prices. If productivity remains robust, the Fed may decide it doesn’t need any more rate hikes.

As such, the main issue for the markets (near-term) is high borrowing costs. Unfortunately, rising productivity and higher real interest rates go hand-in-hand, so if AI technology creates a long-lasting productivity boom, it may also push up long-term interest rates for an extended period of time, weighing on long-term bonds and equity sectors that are interest-rate sensitive.

Going forward we will be looking to further lighten our exposure to equity sectors that are interest-rate sensitive, and in some portfolios we will be looking to reduce risk in our bond fund holdings.

Sincerely,

Jack Bowers

President & Chief Investment Officer