-- Why A Major Federal Debt Crisis Could Be a Long Way Off

Past Viewpoints:Does It Make Sense To Roth-Convert Your IRA In Retirement?

You’ve got a significant amount of money in a traditional (or rollover) IRA, and you’re not thrilled with RMDs (Required Minimum Distributions) that get bigger with each passing year. Does it make sense to "pre-pay" the entire tax liability so that the account can grow tax-free for the rest of your life, and (probably) for another 10 years after it’s passed on to your non-spouse heirs?

It’s not an easy question to answer, but with expectations of future tax rates on the upswing, and with Congress poised to reign in the so-called Stretch IRA (a traditional IRA inherited by a non-spouse heir whose distributions are spread out over the life expectancy of that heir), the idea of doing a Roth conversion is looking more attractive. Your heirs may still be required to distribute inherited IRA assets within 10 years, but at least with tax-free Roth distributions they won’t be forced into a higher tax bracket.

Deciding whether to do a Roth conversion (an option that is open to anyone) is not just about estate planning. To get an idea of whether it makes sense for your situation, consider the following questions: (1) Am I in reasonably good health for my age? (2) Can I pay the conversion tax bill (which will likely range from 25-50% of the amount converted) from non-IRA sources and avoid living expense draws on the Roth account for at least 10 years? (3) Can I do the conversion at a time when my capital gain exposure is low, and without pushing myself into a tax bracket that is much higher than what I expect for my future retirement years? If you answered yes to all three questions, you may want toconsider a Roth conversion.

Regarding that last question, Roth conversions can be done in stages. You can convert portions of an account, matching the added tax liability with years when capital gain exposure is low (or avoiding years when college-age children may need financial aid). If you have plans for IRA charity donations, don’t convert that money because it can already be donated free of tax liability.

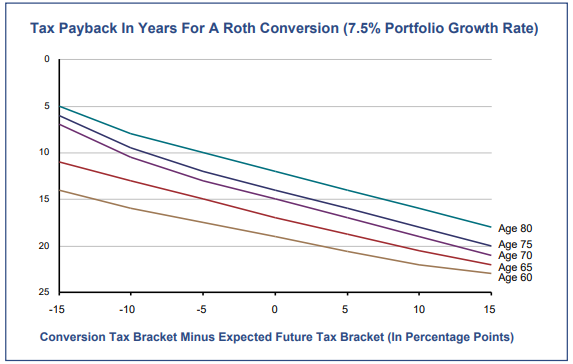

The chart below can give you an idea of what the payback period is for the tax bill that would result from a Roth conversion. The major factors affecting the tax recovery period are taxbrackets and age. Portfolio growth rate matters too, but the impact is relatively mild, so for the sake of simplicity we’re only showing what happens for a 7.5% portfolio growth rate. We’ve assumed that non-IRA money is used to pay the conversion cost so that the full value of the IRA is available to compound tax-free in Roth form.

While there should be no surprise that the payback is longer when your conversion tax bracket is higher than your expected future retirement tax bracket, the impact of age is somewhat counter-intuitive. At age 60, you are bearing the cost of conversion but seeing no payback on future tax savings for at least 10 years. That’s because MRDs don’t kick in until after age 70 1/2 (Congress may soon raise that to age 72). Why not just wait? Well, if your traditional IRA is large, you might need to spread the conversion out over a long period of time to keep your tax bracket from climbing too high. At age 80, payback times are shorter. That’s because MRDs are based on life expectancy, which means they get a lot bigger above age 80, greatly increasing the tax liability of a traditional IRA. Because a Roth conversion eliminates MRDs just as the resulting tax bite starts to become rather large, the resulting payback is relatively short at this age (provided the conversion doesn’t push your tax bracket up too high).

Third Quarter Review

Signs of a slowdown in global growth weighed on U.S. growth stocks in the third quarter. Technology stocks saw weakness as trade friction and the perceived threat of regulation intensified. But it was the health-care sector that took the bigger hit. The group derives a significant share of sales from emerging markets, and could be negatively impacted by the 2020 election. It was no walk in the park for value stocks either. The energy sector got a small lift from the drone attack on Saudi Arabia’s oil infrastructure, but for the quarter it booked large losses, deepening the 12-month plunge that has played out as the world has become glutted with cheap natural gas.

For the quarter, the S&P 500 gained 1.7% on the strength of its large-cap value holdings. But on the mutual fund side it was tough going for active managers. Among Fidelity’s 43 diversified U.S. stock funds, only 5 finished ahead of the index. And a pullback in the Russell 2000 (which lost 2.4% for the quarter) caused the average Select fund to post a fractional loss for the threemonth period. Against that challenging backdrop, the performance of our stock holdings was nothing to write home about.

It was a better story on the fixed income side. The Barclay’s Aggregate U.S. Bond Index rose 2.3% as investors (including many foreigners) sought out the safety and premium yields available from domestic bonds. Our bond fund holdings, which carried about a third less risk than the benchmark, finished only slightly behind the index for the quarter.

Outlook

The U.S. manufacturing sector has begun a mild contraction due to the combined effects of trade friction, economic weakness in Europe and Japan, and the strong dollar. While this raises the risk of a recession, we still think it’s unlikely. The U.S. economy continues to see strength in consumer spending (including home sales), and employment is holding up well despite the long expansion cycle. We can also expect energy prices to remain low and stable. In the past, an oil supply disruption in the Mideast could have been a recessionary knock-out punch, but today we are close enough to energy independence that the drone attack in Saudi Arabia barely registered. Furthermore, the global natural gas glut, created by prolific U.S. exports of LNG, is helping to make electricity less expensive all over the world (while at the same time helping foreign utilities reduce their dependence on oil and coal).

Impeachment proceedings have put some investors on edge, but at this point the risk to the stock market appears quite low. Unless the proceedings overcome long odds and tip the current balance of a Democratic-controlled House and a Republican-controlled Senate in 2020, there’s not likely to be much impact on corporate earnings. Based on recent action in the University of Iowa’s election-betting market (which has a good record of predicting outcomes), the impeachment process appears far more likely to reinforce the Congressional status quo than to alter it.

It’s hard to say if and when we’ll see any relief on the trade front, but eventually some Chinese manufacturers will open factories in the U.S., much like their Japanese counterparts did after the Reagan administration negotiated limits on auto imports in the 1980s. And if Tesla and Costco are any indication, a growing number of American firms should also enjoy success by setting up shop in China. One way or another, the long-term impact of tariffs should diminish over time.

As for portfolio strategy, our current focus is finding areas of opportunity where active management has good odds of success, while adopting a passive approach for market segments where indexing may offer a better risk-reward profile. On the stock side, the rising dollar is creating better opportunities in foreign stocks, which have long sold at a discount to U.S. stocks due to slower growth. Bond-wise, credit spreads have become more attractive in recent months, so we are looking at dialing back interest-rate risk in favor of boosting yield from added highyield bond exposure.

Jack Bowers

President & Chief Investment Officer

P.S. As always we appreciate your feedback. If there is anything we can do to improve your experience as a valued client we’d like to hear from you. In addition, we are accepting new clients this quarter. If you have a friend, colleague, or family member whom you think might benefit from our service please let us know.